From cash to digital euro

Central banks are setting their sights on the future – one in which cash plays only an ancillary role. For instance, the Swiss National Bank (SNB) and Bank for International Settlements (BIS) are testing the possibilities of a central bank digital currency (CBDC). However, this book money would initially only be available for use by financial market participants. The People’s Bank of China (PBOC) is going much further and intends to launch a digital yuan for use by its citizens and foreign tourists as early as the Winter Olympics in February 2022.

The ECB is also dabbling with the idea of a digital euro for use by companies and private households. The course for an eEUR is likely to be set this year: by mid-2021, a decision will be made on whether a concrete project should be initiated. The implications of a digital currency are wide-reaching and numerous practical problems have yet to be solved. The following are some of the key questions (and our answers) with regard to the digital euro.

What on earth is a digital euro?

In future, central bank legal tender will also include currency in digital form. Up to now, the cumulative monetary base (M zero / M0) of a country has consisted of commercial banks’ credit balances held with the central bank, plus coins and banknotes in circulation. With the advent of a digital euro, not just commercial banks, but also private individuals and companies will be able to maintain accounts with the central bank. One’s credit balance held there – in this instance, the ECB – would be available for cashless payments, for example by means of a cash card or smartphone. The precise details have not yet been worked out, but ultimately it would seem that our tried and tested legal tender, i.e. cash in the form of coins and notes, is destined to be morphed into the digital domain.

Why should there even be a digital euro?

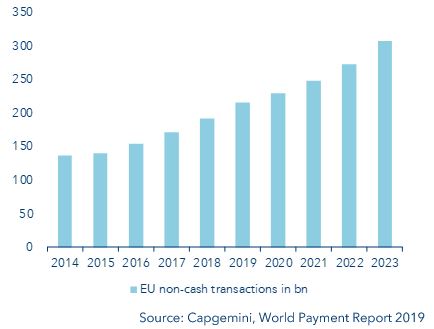

Cashless payments are on a steady rise, and the trend has accelerated due to Covid-19 and the related restrictions on personal mobility. According to a survey by Germany’s Bundesbank, only three out of five consumers still used folding money as a means of payment in 2020. Three years earlier, that cash proportion was still 74%. One thing is clear: cash will lose its importance as we move forward, and countries such as Sweden are showing in which direction this could take us: the Swedes aim to have a cashless economy by 2030.

Cashless transaction in the EU, with projections through 2023

But already today we can use a card or smart-phone for payment purposes

Of course. However, the money comes from your account at a commercial bank and is a claim against that bank. Cash, on the other hand, is a claim against a central bank. So in a cashless world, private individuals and companies would no longer have access to central bank money. This is precisely the situation the ECB wants to avoid through the introduction of the digital euro.

Are central banks like the ECB doing this just because private cryptocurrencies already exist?

The eEUR is not comparable to Bitcoin since the latter is not a real currency in the classical sense. However, the “Diem”, a digital currency under development by Facebook in connection with its “Libra” project, could ultimately be a competitor to any CBDC solutions. A broad consortium has gathered behind this Facebook concept, and plans are for the Diem to be launched before the end of the year. It will primarily serve as a means of payment and thus compete directly with the dollar, euro and other currencies. For this reason as well, the ECB is probably not of a mind to cede the digital currency realm entirely to the private-sector.

Will euro coins and notes be done away with entirely?

According to ECB President Christine Lagarde, cash euros will not disappear after the introduction of eEUR. A digital form of the eurozone currency is not intended to replace cash; both forms of money should exist side by side.

Will negative interest be charged on eEUR deposits?

It remains to be seen whether the digital euro for private individuals and companies will be subject to negative interest. However, the likelihood is that this will be the case, as it would enable the ECB to enforce monetary policy in areas where it is not possible today. Up to now, it has been possible to avoid negative interest charges by hoarding cold hard cash. This essentially defeats the central bank’s intentions – one of which is to incentivise people to spend more on goods, services and investments, which in turn spur economic growth. If the latter were to materialise, it would accomplish exactly what the monetary authorities want. But a two-tier system would also be conceivable, where one interest rate applies up to a certain threshold amount (namely, the same rate banks receive for their ECB credit balances), and negative interest would only be charged on any excess amount.

Will traditional bank accounts disappear in the wake of the eEUR?

Hardly. As the digital euro represents a claim versus the central bank and traditional bank balances are a claim versus one’s “house bank”, safety considerations alone might cause investors to convert their existing credit balances into CBDC on a massive scale. To avoid this, a mechanism could be put in place that prevents all of that cash from being moved into digital form. The ECB is giving thought to the possibility of limiting the role of the digital euro to one of merely being a means of payment. For example, a surcharge could be levied on eEUR credit balances in excess of 3,000 euros. This would prevent too much money from being transferred from commercial bank accounts to central bank accounts. Needless to say, banks offer their customers a wider range of services than just current accounts (e.g. financing, loans, portfolio management, etc.).

Wouldn’t central bank eEUR accounts be a safe haven in the event of a crisis?

The ECB views the digital euro as a modern-day payment alternative and in no way wants to compete with the commercial banks. Equally spoken, if a future financial crisis were to cause a loss of confidence in the banking sector and trigger bank runs, private individuals and companies alike could respond by transferring their cash holdings en masse from their house bank to ECB accounts. This would put credit institutions under tremendous pressure and possibly cause the entire banking sector to founder. At that point, commercial lending would also be choked off, given that bank deposits form the basis for loans. Even negative interest rates would probably not prevent the inflow of funds into central bank accounts in a crisis-of-confidence scenario like this. Hence, further safety-valve mechanisms will be needed to avert precisely such a situation. Most likely, the ECB will not be able to make do without setting an explicit deposit ceiling.

The ECB has summarised all pertinent information regarding the digital euro at:

https://www.ecb.europa.eu/euro/digital_euro/html/index.en.html

Important legal information

This document was produced by VP Bank AG (hereinafter: the Bank) and distributed by the companies of VP Bank Group. This document does not constitute an offer or an invitation to buy or sell financial instruments. The recommendations, assessments and statements it contains represent the personal opinions of the VP Bank AG analyst concerned as at the publication date stated in the document and may be changed at any time without advance notice. This document is based on information derived from sources that are believed to be reliable. Although the utmost care has been taken in producing this document and the assessments it contains, no warranty or guarantee can be given that its contents are entirely accurate and complete. In particular, the information in this document may not include all relevant information regarding the financial instruments referred to herein or their issuers.

Additional important information on the risks associated with the financial instruments described in this document, on the characteristics of VP Bank Group, on the treatment of conflicts of interest in connection with these financial instruments and on the distribution of this document can be found at https://www.vpbank.com/legal_notice_en

Other comments

Thank you very much for your comment regarding our article on CBDCs. Currently VP Bank does neither offer transaction accounts for crypto currencies nor CBDCs. However, feel free to take a look at the other first-rate banking products, which are presented on our website. Should you have any further questions, do not hesitate to reach out to our client service center:

https://www.vpbank.com/en/contact-details

Kind Regards

Gabriel, Group Product Center